Structural steel was first used heavily in buildings about 1885 when the Home Insurance Building in Chicago used it for a framework combined with the more common reinforced concrete. Why so recently? Cost and availability were some factors. Wrought iron had been used frequently for decorations and non-structural applications; cast iron, although strong was brittle, and steel was expensive to make, limiting its use to personal items and tools.

Then, in 1855, the Bessemer Method made the production of steel more efficient and with good tensile strength. This was followed in 1879 by the method of removing phosphorous from steel—increasing its quality and its uses. Steel could finally be produced more cheaply so its production grew. The Rand McNally Building, also in Chicago, was built in 1890 as the first all-steel framed skyscraper. Designed by Burnham and Root, it stood ten stories high and cost $1 million to build at the time. It was demolished in 1911.

From 1875 to 1920 steel production in America grew from 380,000 tons to 60 million tons annually, making the U.S. the world leader. The rapid growth was built on a technological base and the ongoing development of office buildings, factories, railroads, bridges, and more.

In 1913, the Woolworth Building, a 60-story tower, was built in New York. The tallest building in the world at the time, it was a model of steel-frame construction. By 1928, the Chrysler Building, 40 Wall Street, and the Empire State Building fought for the title of the world’s tallest building. The Chrysler Building is still the world’s tallest steel-supported brick building.

What Makes Steel Structural?

Structural steel must meet industry standards for dimensional tolerances and composition. In the United States, steel grades are specified and regulated by ASTM Intl. A wide range of structural steel grades is available, with the most popular being ASTM A572 and ASTM A36. These steel grades, along with other structural steel grades, are mainly used for constructing frames of bridges and buildings.

By use, structural steel accounts for about 47% of all construction materials, weighted heavily by infrastructure use—bridges, especially. One advantage, in this climate concerned age, is that steel can be recycled and reused, avoiding ending up in landfill. Recycling is a method that takes less time and causes less environmental damage than creating steel from raw materials. This is important because steelmaking is energy intensive, accounting for 7% of the world’s carbon emissions in 2020. Steel makers and steel suppliers are carefully evaluating their production processes and business models to reduce net carbon emissions. In 2020, 1.851 tons of carbon were released for every ton of steel produced.

Going Greener

The primary catalyst for carbon neutral and, therefore, “green steel” are government environmental protection policies, which have grown in number in the U.S. since the passing of the National Environmental Policy Act in the 1970s. The 2022 U.S. Inflation Reduction Act is another policy shaping green manufacturing. This act invests $369 billion into domestic energy production and manufacturing activities. Due to its renewable energy focus, the bill is expected to reduce U.S. carbon emissions by 40% by 2030.

Additionally, the Biden Administration announced in September 2022 the U.S. federal government will prioritize the purchase of low-carbon emissions construction materials—including steel—for use in federally funded projects. This comes as an effort to encourage the development of low carbon construction materials within the U.S.

However, as blast furnaces age, mills in certain regions have decommissioned these facilities and replaced them. For example, 70% of steel mills in the U.S. now use EAF (Electric Arc Furnace). As a result, the U.S. releases far less carbon during steel production compared to countries like China and India.

Carbon neutral steel is expected to be more expensive than traditional steel, due to the higher costs of renewable energy sources. However, demand for carbon neutral steel from businesses and consumers is expected to continue growing, making it an evolution of steelmaking. The question is, how much will the market adjust to the cost differential for green, carbon neutral steel? The answer might lie in research being done by numerous companies, projecting the market for steel into the future.

What the Future Holds

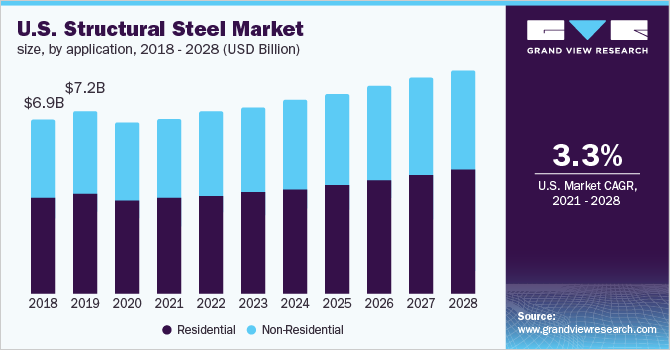

One such firm is Grand View Research. Its analysis shows the structural steel market was valued at $96.94 billion in 2020 and is expected to grow at a CAGR (compound annual growth) of 5.3% from 2021 to 2028. Infrastructural developments, in both developing as well as developed countries, are anticipated to remain primary factors driving the demand for structural steel. The growing housing needs, because of the increasing population across the globe, is also among the key factors driving the product demand.

The market growth was, however, obstructed in 2020 due to the COVID-19 pandemic. According to the World Steel Assn., the demand for finished steel declined by 2.4% in 2020. The pandemic led to factory shutdowns and a shortage of labor, which disrupted the supply chain. The confinement measures froze consumption activities, which reduced demand.

All economies are striving hard to recover from the COVID-19 impact and are spending on infrastructural developments, which are expected to boost the market growth. The non-residential segment emerged as dominant in 2020 with a revenue share of more than 53%.

It is estimated to expand further at the fastest growth rate during the forecast period, owing to increased spending on healthcare facilities, data centers, big-box retail stores, stadiums, airports, and manufacturing facilities. Because structural steel is used heavily in industrial buildings, that sub-segment accounts for the maximum share in the non-residential field.

The residential application segment accounted for the second-highest revenue share in 2020. The product is widely used in housing and residential buildings because of its lightweight and high-strength characteristics, which minimizes the load on the foundation and reduces sub-structure costs.

In addition, due to its excellent flexibility and adaptability in modular construction, it can be dismantled and moved easily, thus maintaining the asset value of buildings. Structural steel can be used in various ways in residential buildings ranging from a single-family house to a big mixed-space building. Moreover, it also provides environmental benefits as it is 100% recyclable with no degradation.

Dealing with Different Data

Another firm, Arizton, uses a different set of data. According to them, the structural steel market is expected to grow at a compound annual growth rate of 6.41% from 2022-2027 and is expected to reach $298.12 billion by 2027 from $205.36 billion in 2021. These figures are partially driven by the environmental aspects mentioned before. The demand for sustainable construction materials is increasing as these materials are environmentally friendly and help the construction industry to practice sustainable development.

Arizton segments the structural steel market into infrastructure, industrial, commercial, and residential. Infrastructure looks like the largest application segment in the structural steel market in the coming years, expected to grow at a rate of 6.65% during the forecast period. In recent years, the demand for improvements in the infrastructure sector is expected to grow significantly due to rapid industrial development and increasing population. Infrastructure development is critical for a country’s economic success; thus, governments invest heavily in infrastructure projects such as trains, roads, electricity, water, and sanitation.

The View from India

The increasing number of green buildings in the country is expected to drive market growth, according to a third research firm, India-based MMR (Maximize Market Research).Government initiatives to improve the housing situation in various countries have increased the demand for structural steel in construction. It also finds the non-residential segment dominated the market with a 54% share in 2021.

The residential segment is expected to grow at a rate of 4% through the forecast period. Steel provides excellent flexibility and adaptability in modular construction, it can be dismantled, moved easily, and maintains the asset value of the building. These are the factors MMR expects to drive the market growth through the forecast period.

The market for structural steel is, obviously, a global market. However, not all countries manufacture steel so the import/export business can be considered a major part of the steel supply chain. Increased usage of carbon steel in the production of construction materials, such as pipes and tubes, and growing applications of carbon steel among various end-user industries are also boosting market growth.

The steady growth of the automotive industry across the globe is driving demand for carbon steel, which is driving revenue growth of the market. In the upcoming years, it is projected that key companies in emerging economies will continue to increase their investment in mining operations and that there would be an increase in demand for low carbon steel.

As with all segments of the economy today, steel production and use is a multifaceted industry, from mining to mills to buildings. Interruptions along the path are more common, as political unrest pops up in nation after nation. Mines in Africa are under attack by rebels, mines in the U.S. are under attack by environmentalists. New technology, such as autonomous mining vehicles, are changing the business model at that end while the demand for steel in heavy equipment pulls the market higher at the construction steel end.

Want to tweet about this article? Use hashtags #construction #sustainability #infrastructure #IoT #edge #futureofwork